Table of Content

Credit scores lower than a 580 can qualify for an FHA loan if they are willing to and able to put down a ten percent down payment instead. Are you still interested in the potential long-term benefits of buying a HUD home? The HUD homes definition sometimes makes potential buyers a little wary of the process and the real advantages of this type of purchase. The general public is able to look at this site, as well as real estate professionals who may be approved to sell this type of property.

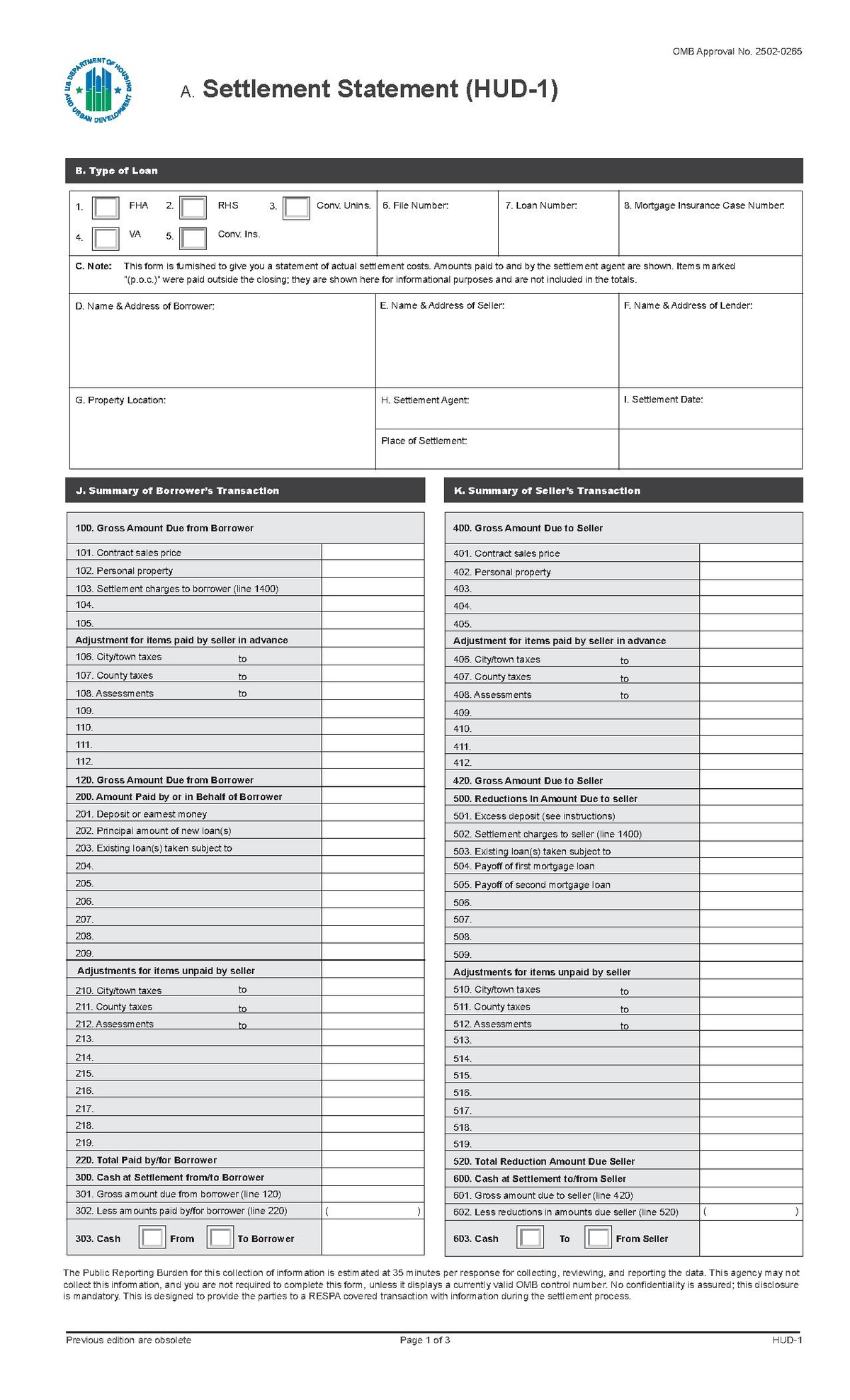

Some homes are move-in ready; HUD monitors them to make sure they’re secure while they sit unoccupied. If you served for at least 90 days of active duty, you meet the minimum service requirement. If you’ve served for at least 90 days of active duty, you meet the minimum service requirement. Monthly debts are recurring monthly payments, such as credit card payments, loan payments , alimony or child support. Generally speaking, FHA loans might be a good fit if you have less money set aside to fund your down payment and/or you have a below-average credit score. A closing statement, also called a HUD-1 statement or settlement sheet, is a form used in real estate transactions with an itemized list of all the costs to the buyer and seller.

For service members

Call your local office of housing and community development or your mayor's office to see if there are any local homebuying programs that could help you. Contact one of the HUD-approved housing counseling agencies. FHA-insured Title I loans may be used for any improvements that will make your home basically more livable and useful.

Look up the Housing Authority in the county you live in to check to see if you meet the income requirements. The website will also list phone numbers to contact someone in the town you are interested in. They will know if there is an opening on the current waiting list as well. Individuals that just receive disability would qualify income-wise.

What happens when HUD takes over a reverse mortgage?

While there’s no minimum credit score required for eligibility, you must be deemed creditworthy. Interest rates are calculated based on market rates, not on your credit score. HUD loans—also called Federal Housing Administration loans—are mortgage loans that are offered by private lenders and insured by the FHA. If a home does not meet minimum standards for health and safety, repairs may be required before a loan will be granted.

These properties are more accessible to low-income households and may come with benefits like prepaid closing costs. Most lenders need 3-6 weeks for the entire loan approval process. Your real estate agent will be familiar with the lenders in the area and what they are offering. Or you can look in the real estate section of your local newspaper – most newspapers list the interest rates offered by local lenders. It is possible to get a loan with a credit score of less than 650. Generally, the credit score required for a personal loan is 550 or higher.

Who Can Get a HUD Loan?

Once you are ready to apply for a Section 184 loan and know that you can qualify for the HUD 184 loan, you can contact an approved lender. Unfortunately, you can’t just go out and find your own lender. In order to use the HUD 184 loan that you qualify for, you have to use a lender from their federally approved list of lenders.

A HUD home presents a realistic opportunity to own your own home for a fraction of the cost of the original list price. When the lender achieves three scores , the central number must be used for the purpose of FHA qualification. When two scores are drawn , the lower number should be used to determine eligibility. You must have a steady income and provide proof of employment.

This means you can’t buy the home and flip it a month later. This is put in place so primary homeowners are able to obtain homes instead of investors who would normally purchase distressed properties. Once you have your home inspection, you’ll be able to make a more educated decision about the price you bid on the home. After the inspection, if you see the home needs a new roof and new windows, you can factor this into your offer. However, not all homes will need extensive repairs or improvements.

You must live in a HUD home for twelve months if you purchase it as an owner-occupant. Those who buy homes with the Good Neighbor Next Door incentive agree to live in the property as a primary residence for a minimum of three years. Ordinarily, homes that need to be remodeled will first need to be purchased and then the owner will need to obtain a construction loan.

You may be eligible for HUD Housing if you have a low to moderate-income, are elderly, or have a disability. There are a variety of different assistance programs available through HUD, so check the website to see which ones you'll qualify for. For most of the programs, you'll need to make 80% or less of the median income in your area.

If you’re purchasing the home as an investor, you’ll have to wait for the initial listing period to pass before making an offer. HUD homes aren’t listed on the Multiple Listing Service like most homes for sale are. To take a look at HUD homes for sale in your area, you should go toHUDHomestore.gov, which is the agency’s official website for these single-family home listings. Once there, you can filter the tool to see HUD foreclosures for sale in your area. Purchasing a HUD home can make homeownership significantly more affordable for you.

5% down payment for a borrower with a credit score of 580 or higher. Investors on HUD purchases must have a down payment of at least 25 percent for single-family residential units. Investors purchasing properties with two to four units must have a minimum down payment of 15 percent.

Then scroll through the list to find the contact information (phone and/or e-mail) for the one in your city. The HUD-1 Settlement Statement is a document that lists all charges and credits to the buyer and to the seller in a real estate settlement, or all the charges in a mortgage refinance. … In transactions that do not include a seller, such as a refinance loan, the settlement agent may use the shortened HUD-1A form.

Some of these programs are also sponsored by your local government, so be sure to do your research at the federal, state, and local levels to ensure you can get the assistance you need. HAs generally receive many more applications for assistance than they are able to accept. FHA loans have been helping people become homeowners since 1934. The Federal Housing Administration - which is part of HUD - insures the loan, so your lender can offer you a better deal. Another perk is the chance to buy a home with a low down payment.

No comments:

Post a Comment